🏦 Credit Risk & Loan Portfolio Analysis

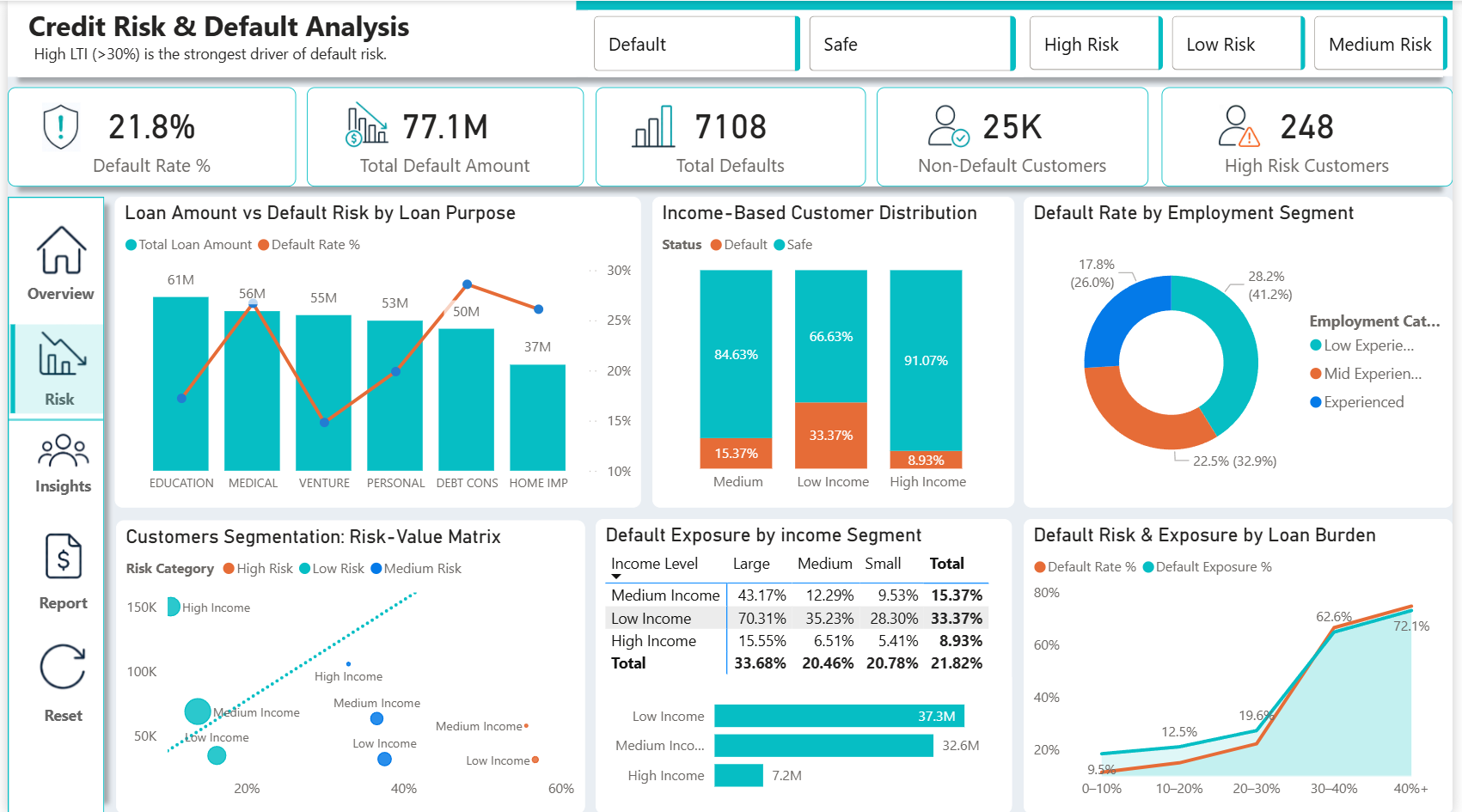

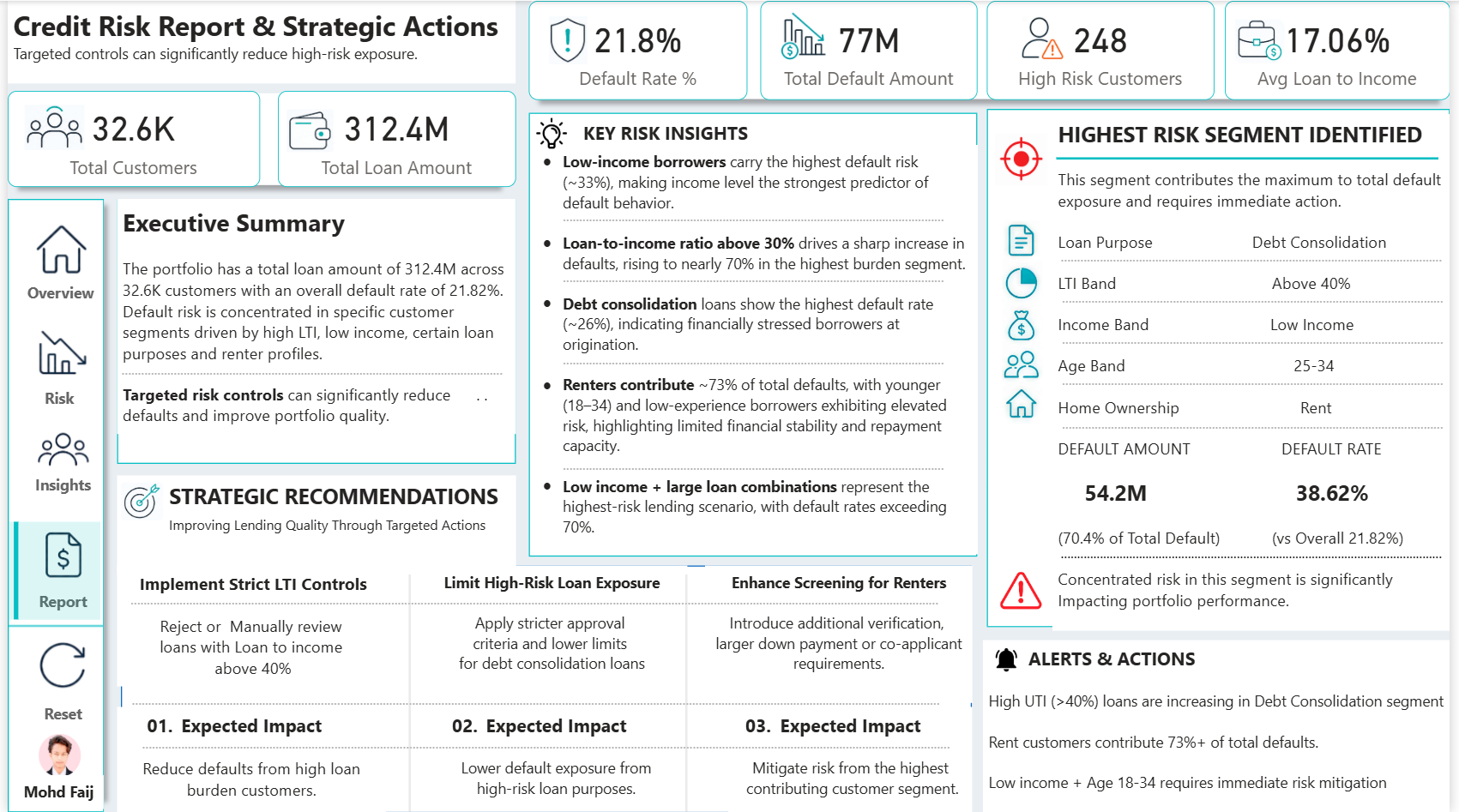

Total Customers

Total Loan Amount

Overall Default Rate

Total Default Amount

High-Risk Customers

Avg Loan-to-Income

The Insight That Changed Everything

The analysis revealed that low-income borrowers taking large loans create a compounding risk — a default rate exceeding 70% in that single segment alone. Yet this group was being approved at nearly the same rate as safer segments.

The risk wasn't just high LTI or low income in isolation — it was their intersection. Identifying this compound risk profile became the foundation for every strategic recommendation in the report.

This segment contributes the maximum to total default exposure

- Low-income borrowers: ~33% default rate — income level is the single strongest predictor of default

- LTI above 30% drives sharp default spike — rising to nearly 70% in the highest burden segment

- Debt Consolidation: ~26% default rate — highest of any loan purpose, signals financially stressed borrowers

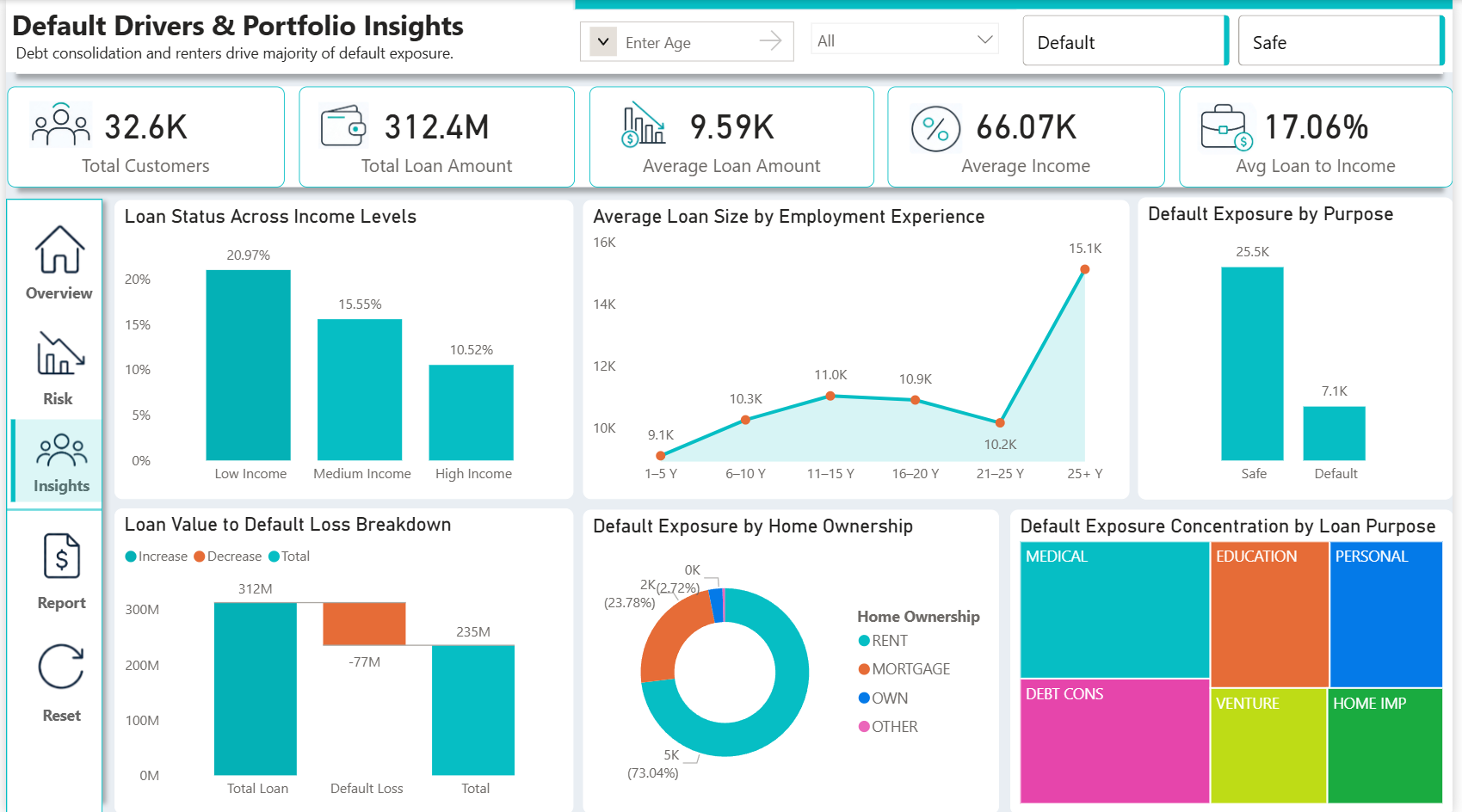

- Renters = 73% of total defaults — younger (18–34) + low-experience profile amplifies risk further

- Low Income + Large Loan = 70%+ default rate — the most dangerous lending combination

- Portfolio loss bridge: ₹312M total loans → -₹77M default loss → ₹235M performing value

- Experienced borrowers (25+ yrs) take larger loans (₹15.1K avg) but with far better repayment history

Live Alerts & Early Warning Signals

- High LTI (>40%) loans are increasing in the Debt Consolidation segment

- Rent customers now contribute 73%+ of total defaults — trending upward

- Low Income + Age 18–34 cohort requires immediate risk mitigation review

-- Default rate by income segment and loan burden SELECT IncomeLevel, LTIBand, COUNT(*) AS TotalCustomers, SUM(CASE WHEN LoanStatus = 'Default' THEN 1 ELSE 0 END) AS Defaults, ROUND( SUM(CASE WHEN LoanStatus = 'Default' THEN 1.0 ELSE 0 END) / COUNT(*) * 100, 2 ) AS DefaultRate, SUM(LoanAmount) AS TotalExposure FROM LoanPortfolio GROUP BY IncomeLevel, LTIBand ORDER BY DefaultRate DESC; -- Highest risk segment isolation SELECT * FROM LoanPortfolio WHERE HomeOwnership = 'RENT' AND IncomeLevel = 'Low' AND LoanPurpose = 'Debt Consolidation' AND LTI > 0.40 AND Age BETWEEN 25 AND 34;

import pandas as pd import seaborn as sns import matplotlib.pyplot as plt # Default rate heatmap – income vs LTI band pivot = df.pivot_table( values='DefaultFlag', index='IncomeLevel', columns='LTIBand', aggfunc='mean' ) * 100 sns.heatmap(pivot, annot=True, fmt='.1f', cmap='RdYlGn_r', linewidths=0.5) plt.title('Default Rate % – Income vs LTI Band') plt.tight_layout() plt.show() # Portfolio loss bridge categories = ['Total Loan', 'Default Loss', 'Net Value'] values = [312, -77, 235] colors = ['#06BEC4', '#E66C37', '#06BEC4'] plt.bar(categories, values, color=colors) plt.title('Portfolio Loss Bridge (₹M)') plt.show()

// Default Rate % Default Rate % = DIVIDE( CALCULATE(COUNTROWS(Loans), Loans[Status] = "Default"), COUNTROWS(Loans) ) * 100 // Composite Risk Score per customer Risk Score = VAR LTIRisk = IF(Loans[LTI] > 0.40, 0.35, IF(Loans[LTI] > 0.30, 0.20, 0)) VAR IncomeRisk = IF(Loans[IncomeLevel] = "Low", 0.30, IF(Loans[IncomeLevel] = "Medium", 0.15, 0)) VAR TenureRisk = IF(Loans[EmpYears] <= 5, 0.20, 0) VAR OwnerRisk = IF(Loans[HomeOwnership] = "RENT", 0.15, 0) RETURN LTIRisk + IncomeRisk + TenureRisk + OwnerRisk // Default Exposure % of Total Default Exposure % = DIVIDE( CALCULATE(SUM(Loans[LoanAmount]), Loans[Status] = "Default"), SUM(Loans[LoanAmount]) ) * 100

1 Implement Strict LTI Controls

Reject or manually review all loans with Loan-to-Income ratio above 40%. Cap approval at LTI 30% for low-income applicants.

Reduce high-burden defaults2 Limit High-Risk Loan Exposure

Apply stricter approval criteria and lower limits for Debt Consolidation loans, especially for renters under 35.

Lower purpose-driven exposure3 Enhanced Screening for Renters

Introduce additional verification, larger down payment requirements, or co-applicant mandates for the rent + low-income profile.

Mitigate highest-risk segment- SQL — Data prep, segment isolation, cohort default analysis

- Python (Pandas, Seaborn, Matplotlib) — EDA, risk heatmaps, loss bridge visualisation

- Power BI — 4-page interactive dashboard with bookmarks, slicers & drill-through

- DAX — Risk score, default rate, LTI band measures, exposure % KPIs

- Dataset — Loan portfolio with 32.6K customer records across income, purpose & ownership attributes